-

Home

- Blog

Blog

- Details

Why Wolverhampton’s Under-34s Are Taking Longer to Buy a Home

It’s no great revelation that young people in Wolverhampton are finding it increasingly difficult to buy a home. Rising living costs, modest wage growth, and stricter mortgage lending rules have all contributed to a noticeable shift in the housing landscape. For many under 34, homeownership feels more like a long-term goal than a near-term reality.

But just how challenging is the situation? And what might the future hold for younger Wolverhampton residents trying to take that first step onto the housing ladder?

A Snapshot of Housing Realities for Wolverhampton’s Young Adults

Across Wolverhampton, there are approximately 105,141 households.

Of those, only 2.6% are headed by people aged 16 to 24, and 13.8% by those aged 25 to 34. Interesting when compared with the national averages of 2.6% and 13.5% respectively.

Let’s dig into how these young residents are actually living.

For 16 to 24-year-olds in Wolverhampton:

- Owned outright: 3.0%

- Owned with a mortgage: 7.2%

- Social housing: 44.2%

- Private renting: 45.6%

(Nationally: Owned outright 3.6% / Owned with a mortgage 10.2% / Social housing 22.8% / Private rented 63.5%)

For 25 to 34-year-olds in Wolverhampton:

- Owned outright: 4.0%

- Owned with a mortgage: 27.7%

- Social housing: 30.1%

- Private renting: 38.2%

(Nationally: Owned outright 4.1% / Owned with a mortgage 35.5% / Social housing 17.7% / Private rented 42.7%)

These figures reveal a clear picture: homeownership is happening later than in the 1980s, and renting, especially privately, is the norm for many young adults in Wolverhampton.

Why Is This Happening?

There’s a widespread belief that rising house prices and stagnant wages are locking young people out of the property market. And while that perception isn’t without merit, the reality is more complex.

Yes, property values have increased, and saving for a deposit is undeniably challenging for many. The % of deposit (a minimum of 5%) hasn’t changed, yet the size of the deposit needed in pound notes is larger than ever, especially for those balancing increases in rent, bills, and student loans. Mortgage lending criteria have also tightened in recent years, creating additional hurdles.

However, some numbers challenge the narrative. Real wages today are 23.8% higher than they were in 2000, meaning people are, on average, earning nearly a quarter more in real terms than 25 years ago. That’s a crucial point often overlooked in media headlines.

Yet, while ‘real’ incomes may be higher, the proportion of household income spent on mortgage payments tells a different story. In 2002, the average first-time buyer household spent 24.6% of their income on mortgage costs. Today, it’s 34.9%, a noticeable jump, though still below the 44.9% peak seen in 2007 before the financial crisis.

So, while incomes have improved, affordability has been squeezed by rising house prices, higher deposit requirements, and costlier monthly repayments. The perception that homeownership is harder now isn’t without foundation, it’s just that the causes are layered, not linear.

The Changing Face of Wolverhampton First-Time Buyers

It’s easy to romanticise the past, where buying a home in your early 20s was the norm. But the reality is that this was largely limited to previous generations. In the 1980s, the average first-time buyer was around 26 years old. Today, it’s 31 (and 34 in London).

This isn’t unique to Wolverhampton and the UK. In fact, many developed countries have seen similar trends. In Germany, for instance, it’s common for people to rent into their late 30s or early 40s before buying, often when they have greater financial security and a larger deposit, resulting in less mortgage debt overall.

It’s a slower start, but potentially a more stable one in the long term.

The Silent Power of £8.6 Billion in Wolverhampton

One of the most overlooked aspects of Wolverhampton’s property future lies in the wealth of its older generations. Across Wolverhampton, the over-50s collectively hold over £8.6 billion in property equity.

Many of them bought their homes decades ago when prices were significantly lower. As they begin to downsize or pass on their estates, this could unlock a huge transfer of wealth to younger generations.

In Wolverhampton, where family ties often run deep, this could be the key to many younger residents finally stepping onto the property ladder, not by scraping a deposit together alone, but through inheritance or family assistance.

So What’s Next for Wolverhampton’s Young Homebuyers?

The outlook isn’t all negative. While current ownership rates among under-34s are low, it doesn’t mean they’re permanently shut out of the market. In many cases, it’s just a matter of timing. The real shift will likely come from a combination of cultural change (more young people willing to wait) and financial support from older generations.

Delayed doesn’t mean denied.

With more young people getting financially prepared, and intergenerational wealth set to play a bigger role, Wolverhampton could see a gradual rise in homeownership among younger adults in the years ahead.

The challenge is real, but so is the potential.

Wolverhampton’s younger generation aren’t being locked out forever. They’re just waiting longer to find the right door to walk through.

What do you think? Is this the calm before the next wave of first-time buyers?

- Details

Why it's back in fashion (and why it never really went out)

In an age of towering new build flats and sprawling three-storey town homes, there is something refreshingly honest about a bungalow. No stairs. No split-level gimmicks. Just a simple, all on one level home that offers practicality, privacy, and increasingly, prestige.

If you had asked the average house hunter a decade ago to rank their dream home, the bungalow might have appeared low on the list. Today, that story is changing fast. Demand is outstripping supply, prices are rising faster than many other property types, and in some parts of the country, bungalows are attracting bidding wars that would make some posh Home Counties estate agents in the ‘Race for Space in 2021’ blush.

But what’s behind this resurgence? Why are bungalows back in fashion, especially with those in their 40s and 50s? And more importantly, what do buyers (and sellers) need to understand about this deceptively simple property type?

The Underdog of British Housing

Let's start with a truth rarely spoken aloud. Bungalows have long been the butt of architectural snobbery. They are often dismissed as the choice of the elderly, a relic of the pre- and post-war property boom, or worse, a temporary fix while something ‘better’ comes along.

Yet, this perception masks the fact bungalows are rare, valuable, and often sit on plots that developers would kill for.

While two-storey semis and terraces fill the suburbs, bungalows occupy wide plots with generous gardens, driveways, and that all-important future potential. Knock it down, extend outwards or upwards, or modernise; the options are endless.

Why Buyers Love Them

Retirees don't just fuel the resurgence in bungalow demand, although they remain a core demographic. Increasingly, we're seeing younger 40 and 50-somethings, people with mobility considerations, and even developers entering the market.

There are five key reasons why buyers are falling back in love with bungalows:

- Single-Level Living

No stairs might sound like a small thing until you try living without them. Whether you've got toddlers, teenagers, ageing knees, or just a desire for flow, bungalows make sense.

- Future-Proofing

Buyers are thinking long-term. A couple in their 50s might be in fine health now, but they're looking for a home they can grow old in without having to move again.

- Extension and Rebuild Potential

Many bungalows sit on plots double the size of today's modern homes. That opens the door to rear extensions, loft conversions, or even total redevelopment, subject to planning.

- Peace and Privacy

With no neighbours above or below, bungalows offer a quieter, more serene lifestyle. That's something people truly value post-lockdown.

- Scarcity

Very few bungalows are built today. National housebuilders focus on density, and single-storey homes don't stack up (literally) for profit. That means the ones that exist are in short supply, and we all know what happens when supply is short.

What the Wolverhampton Market Is Saying About Bungalows

Examining the data from the last two years, we can begin with new listings.

A total of 468 bungalows came onto the market in Wolverhampton, accounting for 6.4% of all new property listings in the area. This figure is interesting when compared to the national UK average, where 7.9% of properties listed were bungalows.

Next, let’s turn our attention to sales performance and prices achieved.

In that same two-year period, 267 bungalows in Wolverhampton were sold and completed.

The average sale price of a Wolverhampton bungalow was £284,451, working out at £329 per square foot. For comparison, 4,380 houses and flats sold in the same period with an average price of £245,097, equating to £241 per square foot.

This clearly shows that bungalows in Wolverhampton command a significantly higher price per square foot compared to other types of properties.

Finally, let's examine saleability, which is the percentage of properties that sell, from exchanging contracts to completing and moving once they’re listed.

In Wolverhampton, 61.1% of bungalows that came off the market ended up selling and moving (the remainder left the market unsold). That compares to 62.8% for flats and 66.5% for houses. Nationally, the picture is slightly different. 60.6% of bungalows sell and complete, but only 46.3% of flats and 56.2% of houses do the same.

These figures underline the enduring appeal and substantial value of bungalows in the local market.

Wolverhampton is WV1/2/3/4/6/10/11.

Advice for Wolverhampton Bungalow Sellers

If you’re the owner of a Wolverhampton bungalow, especially in a sought-after area, and considering moving in the not-too-distant future, maybe now is the time to have a conversation?

If you were concerned about not being able to find a home, if you would put your bungalow on the market and find a buyer, then we operate an 'off market' service at our agency where we can discreetly find you a buyer, without a for sale board, and then ask them to wait as long as it takes for you to find your next home, even if that takes months and months. And at any time during the process, if you change your mind before the legal work is completed with the solicitors, there will be no cost whatsoever.

However, pricing it right is crucial. Go too high, and you risk scaring off the serious buyers. Go too low, and you invite developers who see the plot, not the home.

An experienced agent will know how to position your bungalow to attract the correct type of buyer, whether that's a family, a downsizer, or someone planning their 'forever home'.

Final Thoughts

The British love affair with bungalows is being rekindled. Quietly, steadily, and with increasing confidence, these single-storey homes are proving they were never just for pensioners. They’re practical, adaptable, and crucially desirable.

Because when it comes to bungalows, one thing’s for sure: we may not be building many. In fact in the last year alone only 1.88% of all new homes were bungalows, but despite this the appetite for them is only going up.

- Details

As we are now half way through 2025, it's certain the Wolverhampton housing market has been more restrained than the post pandemic 24 months of summer 2020 through to July/August of 2022, and I believe that the ‘steady as she goes’ outlook will continue into the rest of 2025 and beyond.

As we always say in our Wolverhampton property market updates, home ownership is a medium to long-term investment, so we feel it’s always important to measure what has happened to Wolverhampton house prices over those medium to long terms.

Since the summer of 2005 the average Wolverhampton homeowner has

seen their property’s value rise by an average of 47%.

This is significant as house prices are a national fascination and sub-consciously tied into the perceived health of the UK economy. Most of that 47% gain has come from the overall growth in all Wolverhampton property values, while some of it will have come about by modernising, extending or developing their Wolverhampton home.

Analysing the different types of property in Wolverhampton and the profit made by each type, it makes interesting reading:

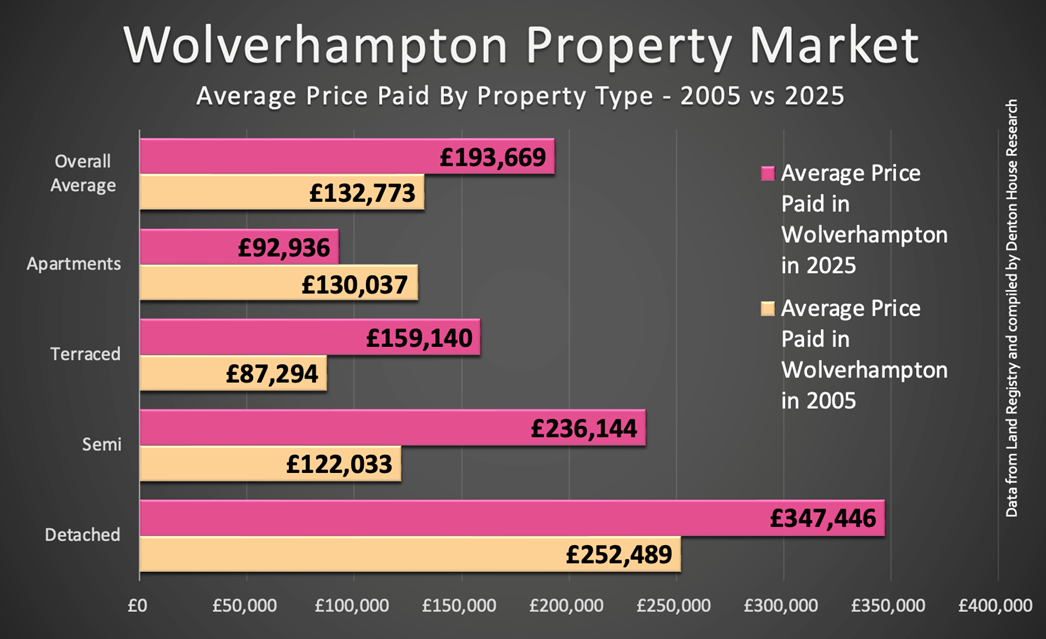

- Overall average for all homes in Wolverhampton. The average price paid for all homes in Wolverhampton in 2005 was £132,773. Now it's 2025, and it has risen to £193,669. This is a total profit of £60,896 (which is £3,045 profit per year per home or an annual growth of 2.4% per year).

- Apartments in Wolverhampton. The average price paid for apartments in Wolverhampton in 2005 was £130,037. Now it's 2025, and it has fallen to £92,936. This is a total loss of £37,101 (which is £1,855 loss per year per home or an annual loss of -1.4% per year).

- Terraced/Town Houses in Wolverhampton. The average price paid for all town house/terraced houses in Wolverhampton in 2005 was £87,294. Now it's 2025, and it has risen to £159,140. This is a total profit of £71,846 (which is £3,592 profit per year per home or an annual growth of 4.1% per year).

- Semi-Detached Homes in Wolverhampton. The average price paid for all semis in Wolverhampton in 2005 was £122,033. Now it's 2025, and it has risen to £236,144. This is a total profit of £114,111 (which is £5,706 profit per year per home or an annual growth of 4.7% per year).

- Detached Homes in Wolverhampton. The average price paid for all detached homes in Wolverhampton in 2005 was £252,489. Now it's 2025, and it has risen to £347,446. This is a total profit of £94,957 (which is £4,748 profit per year per home or an annual growth of 1.9% per year).

However, we can’t forget there has been 77% inflation over those 20 years, which eats into the ‘real’ value (or true spending power of that profit) … so if we consider inflation since 2005, the true ‘spending power’ of that profit has been lower.

- Overall average for all homes in Wolverhampton. The total 'real profit' (i.e. after inflation has been deducted) for the average Wolverhampton home is £34,366 for the last 20 years. This equates to £1,718 'real' profit per annum.

- Wolverhampton Terraced/Town House homes. The total 'real profit' (i.e. after inflation has been deducted) for the average Wolverhampton town house/terraced home is £40,545 for the last 20 years. This equates to £2,027 'real' profit per annum.

- Wolverhampton Semi-Detached homes. The total 'real profit' (i.e. after inflation has been deducted) for the average Wolverhampton semi-detached home is £64,397 for the last 20 years. This equates to £3,220 'real' profit per annum.

- Wolverhampton Detached homes. The total 'real profit' (i.e. after inflation has been removed) for the average Wolverhampton detached home is £53,587 for the last 20 years. This equates to £2,679 'real' profit per annum.

Therefore, the profit for an average Wolverhampton home over the last two decades, adjusted for inflation, stands at £1,718 per year.

We wanted to show you that despite the 2008/09 Credit Crunch property market crash, which saw Wolverhampton property values plummet by 16% to 19% over 18 months, Wolverhampton homeowners have still fared better over the long term than those renting.

Looking ahead, a common question I get asked is about the future

direction of the Wolverhampton property market.

The main influence on maintaining house price growth in Wolverhampton over the medium to long term will be the construction of new homes (on the supply side) and employment and interest rates (on the demand side). Although we have yet to get the official figures for 2024, independent sources indicate that the number of new households is expected to be around 217,900. Bearing in mind the annual need is for 300,000 new UK households to meet demands - arising from factors such as increased life expectancy, immigration, and later cohabitation - it’s clear that demand will continue to exceed supply unless the government heavily builds council houses.

This can only be good news for Wolverhampton homeowners.

What about Wolverhampton landlords, though?

Even though the quantity of landlords selling up their rental portfolios has increased in the last couple of years and the number of landlords purchasing buy-to-let properties is lower than in the last couple of decades, there is still margin net growth in the size of the private rented sector each year. This is all notwithstanding landlords facing higher taxes. The fact is many Wolverhampton landlords continue to be keen on expanding their rental portfolios in the medium to long term.

Many of the 20 and 30 something’s of Wolverhampton view renting as a choice that offers flexibility and options that homeownership does not provide. This means that demand for rentals will keep rising, allowing landlords to enjoy capital appreciation and rising rents. However, Wolverhampton buy-to-let landlords must accept more considerate strategies to maintain profitable returns from their investments.

As a Wolverhampton buy-to-let landlord, the issue for you is how to

ensure this growth continues.

Up until 2017, generating profits from buy-to-let property investments was like falling off a log. Since then, with changes in legislation and taxation, the balance of power, achieving similar returns will be more effortful. Over the past 8 years, we have observed the evolution of agents from mere rent collectors to tactical rental portfolio managers. We, along with a select number of agents in Wolverhampton, are skilful at providing strategic and comprehensive portfolio leadership. This service offers a structured overview of your investment goals across short, medium and long-term horizons, focusing on your expected returns, yields and capital growth. If you seek such advice, feel free to contact your current agent or us directly at no cost or obligation.

- Details

In early 2023, most property forecasters anticipated a significant downturn in the UK housing market over the following two years. Halifax predicted an 8% drop in house prices, Savills went further at 10%, and Nomura Bank predicted a fall of up to 15%. While these gloomy forecasts grabbed headlines, the actual data told a different story. According to the Land Registry…

UK house prices are 1.76% higher today than in January 2023, and Wolverhampton house prices are 4.14% higher.

Now, as we are halfway through 2025, many are asking the same question again: will house prices crash this year? Based on current data and trends, the answer is no.

The first thing to note is that although there have been some slight dips in the national averages in early 2025, the falls have been modest. Nationwide reported a 0.8% drop in June (the most significant monthly dip in two years), and the Land Registry figures for April showed a 2.8% annual fall. However, this needs to be put into context. These figures follow a period of exceptional growth during the pandemic years; one shouldn’t expect the market to collapse, and it is now normalising rather than collapsing. Rightmove, which tracks asking prices rather than completed sales, reported a 0.3% drop in June, citing an increase in supply and fading of the stamp duty boost.

Also, Denton House Research uniquely track the £/sq.ft figures at the sale agreed date in the UK. The £/sq.ft figures track the Land Registry five months in advance with a 98% correlation. This means we know what will happen to the published Land Registry house prices five months in advance with a very high level of certainty. Five months ago, the pound per square foot for UK home sales agreed was at £338.67, and today it stands at £346.25 per square foot. Therefore, based on this calculation, UK house prices should be 2.24% higher by January than they are today. None of these points point to a crash.

Looking at the total number of property sales in Wolverhampton…

In the first six months of 2024, 1,509 Wolverhampton homes were sold subject to contract. In 2025, the figure climbed to 1,597 ... a sign of growing confidence in the market.

Wolverhampton – WV1/2/3/4/6/10/11.

In fact, at the start of the year, most forecasters expected prices to rise moderately this year. Savills and the HomeOwners Alliance both project growth of around 4% in 2025. Zoopla has forecast a more cautious 2.5% rise, and Knight Frank predicts a similar increase. Capital Economics anticipated average house price growth of around 4% per year between 2025 and 2027. The consensus across the industry is for stability or a modest recovery, rather than a dramatic decline.

A key reason for the relative resilience of Wolverhampton house prices is the low mortgage rates.

After climbing to over 6% in 2023, rates have stabilised and are expected to continue to fall gradually through 2025. Many lenders have already dropped their fixed-rate deals below 4.5%, and further reductions are likely if the Bank of England continue to cut its base rate later in the year. This shift in affordability is expected to improve buyer sentiment and support price levels.

Crucially, the UK labour market remains strong. Unemployment is low, currently sitting at around 4.6%, and wage growth is holding steady at 5.2% per year. This means that most households can manage their mortgage payments, even with higher interest rates. There is little sign of the kind of financial stress that forces mass sales or repossessions, which typically precede major house price crashes.

Another critical factor is the increasing regulation of mortgage lending over the past decade. Since the introduction of the Mortgage Market Review in 2014, borrowers have had to demonstrate that they can afford repayments at interest rates significantly higher than those they are currently paying. This stress testing was designed to create market resilience, and it has been effective. Even at the height of ultra-low rates, new borrowers had to demonstrate that they could afford repayments of 6.5% or 7%. Now that rates have risen, most are already well-equipped to manage the change. The average stress test rate in 2024 was 7.5% to 8%, and borrowers continue to pass these checks.

There’s also more balance in the Wolverhampton property market.

There has been a rise in the number of Wolverhampton homes for sale with 1,090 available today, up from 1,068 in July 2023. Meanwhile, buyer enquiries have also increased.

Wolverhampton city centre + 3 miles.

This subtle increase in the supply of Wolverhampton homes on the market offers Wolverhampton buyers more choice and has helped prevent bidding wars that inflate prices. Yet demand remains strong, supported by population growth, longer life expectancy, lifestyle changes, and the ongoing desire for homeownership. This equilibrium of supply and demand is stabilising prices, not sending them into freefall. You see, one of the main reasons UK house prices dropped in late 2007 was the high level of homes on the market. In July 2007, there were 2,413 homes for sale in Wolverhampton!

Meanwhile, the rental market is adding another layer of support. High rents have prompted many tenants to consider buying as a more cost-effective long-term option. This has boosted first-time buyer numbers, especially in areas where house prices remain relatively affordable, like Wolverhampton. Some Wolverhampton landlords are also exiting the market, which reduces rental stock, drives up rents further, and makes buying more appealing.

Of course, there are variations across the UK. Some parts of London and the South have seen a softening in house prices over the last few years, as affordability pressures and changes to stamp duty and landlord taxation have taken a greater toll. However, many regions, particularly those in the North of England, Northern Ireland, and parts of Scotland, continue to experience modest house price growth. Regional disparities will always exist, but they don't change the national picture, which is one of moderation, not meltdown.

Could a house price crash still occur?

It's not impossible, but the necessary conditions are not present. To see a genuine crash, we would need a perfect storm: a sharp rise in unemployment, a sudden spike in interest rates, a collapse in mortgage availability, and a wave of forced sales. None of those elements is currently on the horizon.

Even the risks that do exist, i.e. slower-than-expected rate cuts, changes to government housing policy, or economic shocks from abroad, would likely lead to stagnation or small dips, rather than a crash. The foundation of the UK housing market is far stronger than it was in 2008 or the late 1980’s. There is no subprime mortgage crisis, no rampant overborrowing, and no glut of unsold new builds.

In conclusion, although the UK housing market in 2025 is not without its challenges, the data and trends indicate a firm direction towards stability. A crash remains highly unlikely. Most regions are expected to experience slow but steady growth. Some pricier areas may dip slightly. But overall, the narrative for 2025 is one of cautious optimism. Buyers and sellers alike would do well to tune out the crash headlines and focus on what the numbers are saying.

If you're planning to move, buy, or invest this year, opportunities abound, especially if you understand your local market and take a long-term perspective. This is a normalising market, not a collapsing one.

- Details

If you have ever thought about selling your Wolverhampton home, chances are you have been tempted to push the asking price a little higher than advised. After all, it’s your biggest tax free asset. A few extra thousand on the asking price of your Wolverhampton home sounds like a smart move, doesn’t it?

But here’s the rub: in property, chasing too much can often mean getting nothing at all.

Since the start of 2020, over 6,386 homes, listed for sale in Wolverhampton were withdrawn from the market unsold. And while some may blame timing or market conditions, in many cases the underlying problem is much simpler, the asking price was too high from the outset.

Let us explore how this has unfolded, why it’s happening, and most importantly, what you can do as a Wolverhampton homeowner to avoid falling into the same trap.

The Temptation to Overprice and Why it Backfires

When estate agents come round to pitch for your business, it’s not uncommon to hear different figures. One might suggest £285,000. Another £300,000. Then someone walks in and says £325,000, no hesitation, no caveats.

It’s flattering. It’s exciting. And it’s often a trap.

Some agents know exactly what figure will win your instruction, even if it has little grounding in what the market will pay. They don’t need to sell the home straight away they just need it on the books.

The Wolverhampton Numbers Don’t Lie

Let’s look at the hard data for the WV1-4, WV6, WV10 and WV11 postcode districts. Of the homes that left Wolverhampton estate agents’ books, what percentage of them withdrew from the market without selling?

2020

- Of the 3,602 Wolverhampton homes that came off agent's books:

- 2,349 of them sold & exchanged contracts (i.e. the homeowners moved),

- and the remaining 1,253 of them didn’t sell (i.e. 34.8% failed to move home).

2021

- Of the 3,885 Wolverhampton homes that came off agent's books:

- 2,792 of them sold & exchanged contracts,

- and the remaining 1,093 of them didn’t sell (i.e. 28.1% failed to move home).

2022

- Of the 3,384 Wolverhampton homes that came off agent's books:

- 2,467 of them sold & exchanged contracts,

- and the remaining 917 of them didn’t sell (i.e. 27.1% failed to move home).

2023

- Of the 3,501 Wolverhampton homes that came off agent's books:

- 2,185 of them sold & exchanged contracts,

- and the remaining 1,316 of them didn’t sell (i.e. 37.6% failed to move home).

2024

- Of the 3,679 Wolverhampton homes that came off agent's books:

- 2,368 of them sold & exchanged contracts,

- and the remaining 1,311 of them didn’t sell (i.e. 35.6% failed to move home).

2025 YTD

- Of the 1,487 Wolverhampton homes that came off agent's books:

- 991 of them sold & exchanged contracts,

- and the remaining 496 of them didn’t sell (i.e. 33.4% failed to move home).

In total, that’s 6,386 homes in Wolverhampton since January 2020 that came to market yet never sold. Most of those were overvalued and withdrawn in frustration. Nearly all were likely overpriced in comparison to what buyers were willing to pay at the time.

This is not a coincidence. It’s a pattern.